Beyond Loans — Credit as Price, Collateral, and Code: Part I

Prologue: A coffee, a card, a perp

You tap for a coffee. Somewhere, a card network authorizes a payment, your bank promises to fund it later, and the café gets a message it can trust today. No coins move between you two in that moment; accounting does. That night, a batch closes and money finally travels. A few hours later, an on‑chain trader opens a perpetual futures position with 10× leverage. Again, no assets move between counterparties with every price tick; the system keeps score until a boundary is reached. Same story, different rails. The invisible thread is credit—sometimes explicit, sometimes implicit, sometimes just the promise that when needed, there is cash in the room. This series is about that thread: how we price it, how we secure it, and how code is changing what “settlement” even means.

Part I — Pricing Credit: From Rates to Risk

TL;DR A loan’s rate is not a generic “fee for borrowing.” It is the cash price of uncertainty. Under the hood it combines the time value of money, the lender’s own cost of running the product, the expected loss from borrowers who won’t pay, a return on capital set aside for bad times, and a margin for competition and model error. Change the risk, change the price.

We can say this without jargon. In plain terms: the rate has five components. The first is the risk‑free baseline—what money earns with almost no risk over the same period. The second is funding and operations—the cost of deposits or wholesale funding, the salaries, the software, the compliance. The third is the expected loss from defaults in an average year. Risk teams compute this as EL = PD × LGD × EAD, where PD is the probability of default, LGD is the loss given default after recoveries/collateral, and EAD is the exposure at default. The fourth component is a capital charge—the return required on capital held for recessions and accidents. The fifth is margin.

A small example makes it concrete. Take a €10,000, one‑year loan. Suppose the risk‑free rate for the duration is 3% and running the product costs another 1%. If the risk team believes two out of a hundred similar borrowers will default (PD = 2%) and that, after selling collateral and collecting what can be collected, the average loss is forty cents on the euro (LGD = 40%), then across the whole book the expected loss is 0.02 × 0.40 × €10,000 = €80, or 0.8% of principal over the year. Add a modest 0.5% for capital and 0.7% for margin and you land near 6.0%. Now change only one fact: the borrower pledges a car you can seize and sell, so LGD falls to 10%. Expected loss drops to 0.2% and the fair rate glides toward 5.4%. Capital charge covers unexpected loss (tails), not the average loss already priced in EL.

In practice, each ingredient moves for different reasons. PD falls when underwriting improves—verifiable income, lower debt‑to‑income, cleaner payment history. In on‑chain systems, PD rhymes with the reliability of liquidation: good oracles, healthy order books, a live chain. LGD shrinks with real control over cash flows—first‑priority liens and guarantees in TradFi, over‑collateralization and repayment sinks that get paid before anyone else in DeFi. EAD is structural: amortizing loans dwindle over time; revolving lines can peak late; leveraged positions on‑chain have a special kind of exposure—the notional at risk during the seconds it takes to liquidate. A useful rule of thumb in volatile markets is latency VaR: expected price move × exposure × liquidation delay. Maintenance margins should be set so that, even across that delay, losses are still covered—or an insurance fund must catch what spills over.

Two loans with the same expected loss can still deserve different prices because of tails. Expected loss is the average. Lenders also hold capital for the unexpected: clustered defaults in a downturn, a frozen bridge, an oracle that goes out of tolerance. That capital expects a return. Futures markets make this explicit with initial and variation margin plus a default fund; consumer lenders do it implicitly by targeting a return on economic capital. If one pool has fat‑tailed outcomes and another doesn’t, the one with fatter tails will carry a higher capital coat of paint even if the expected‑loss coat is the same thickness.

This is where TradFi and DeFi feel different while solving the same equation. TradFi mostly prices people and paper: PD is about willingness and ability to pay; LGD is about legal priority and recoveries; EAD follows the contract schedule. DeFi mostly prices collateral and code: PD is about whether the liquidation machine keeps up; LGD is the shortfall after selling collateral (plus any insurance); EAD is the notional during liquidation or bridging. Both are trying to make expected loss small and capital affordable, just with different levers.

If you carry one idea forward from Part I, carry this: the rate is a story about risk that can be measured and moved. Lower PD by knowing your counterparty or by making misuse structurally impossible. Lower LGD by taking collateral you can truly control or by routing repayments to yourself first. Shape EAD by choosing structures that shrink exposure when it matters. The math is compact; the art is in the design.

Interlude — Settlement Taxonomy, Non‑deliverables, and Actor Map

Before we compare products, it helps to lock down the language. Settlement has two layers that sit at right angles. The first is the mechanism—how and when transfers are finalized. The second is the guarantee—the promises or safeguards that make that timing safe. “Guaranteed solvency” belongs to the second layer; it isn’t a timing rule, it’s the property that lets slower or more flexible timing work without creating unpayable obligations.

On mechanisms: at one end is instant or atomic settlement. Value and title change hands together, and if either leg fails, nothing happens. This is delivery‑versus‑payment and real‑time gross settlement: a clean swap with no exposure carried across time. A step away from that is escrow‑mediated settlement. Funds or assets lock immediately but do not release until a condition is proven—delivery confirmed, a dispute window expires, an oracle attests to a state. No one extends credit in the meantime; risk is parked in escrow rather than on a counterparty’s balance sheet.

Most day‑to‑day finance relies on deferred net settlement (DNS). Obligations are fixed now, but cash moves on a schedule—end‑of‑day batches, T+2 cycles, month‑end nets. Because many cash flows point both ways, the system nets them down to smaller transfers. Sometimes a third party layers credit on top—card issuers and BNPL firms pay the merchant today and collect from the buyer later—but the settlement layer itself is just batching and netting.

Then there is event‑driven or boundary settlement. Instead of moving cash at every interim event, the system keeps score internally and only moves real money at boundaries such as closing a position or withdrawing funds, or when risk limits are hit and liquidation is required. Timing becomes stochastic—the market decides when boundaries are reached—but the rules are deterministic: margins, oracles, liquidation incentives, and priority of payouts define what happens when a boundary is crossed. Finally, in markets that concentrate many bilateral trades, novated CCP settlement inserts a central counterparty between everyone else—becoming buyer to every seller and seller to every buyer—and runs multilateral netting with initial/variation margin, default funds, and auctions.

There is a cousin to these mechanisms that shows up everywhere: non‑deliverable agreements. Some contracts never require transfer of the underlying asset at all; they settle purely in cash off a reference price or index. A non‑deliverable forward on USD/KRW pays the difference in dollars at maturity; cash‑settled options and many index futures do the same. On‑chain, most perpetuals are by design non‑deliverable—the reference is a price index, and the settlement asset is a stablecoin. Non‑deliverables simplify custody but make pricing integrity the critical dependency: if the reference price is wrong, so is the payout. Oracles, dispute windows, and robust indices therefore sit squarely in the guarantee layer.

Now to guarantees—the layer that makes those mechanisms safe. Finality means that once a transfer is marked complete, it cannot be unwound except by a fresh transaction or a court order. Reversibility is the mirror image for conditional flows: when conditions are not met, value reliably returns to its origin (escrow release, chargebacks, dispute rules). Priority fixes who gets paid first; it is a legal assignment in paper systems or a programmed repayment sink on‑chain. And guaranteed solvency is the core invariant behind boundary models: at any boundary event, the system can meet its obligations from posted buffers, liquidation proceeds, and insurance, with any remaining shortfall pre‑allocated to a funded waterfall rather than pushed onto outsiders.

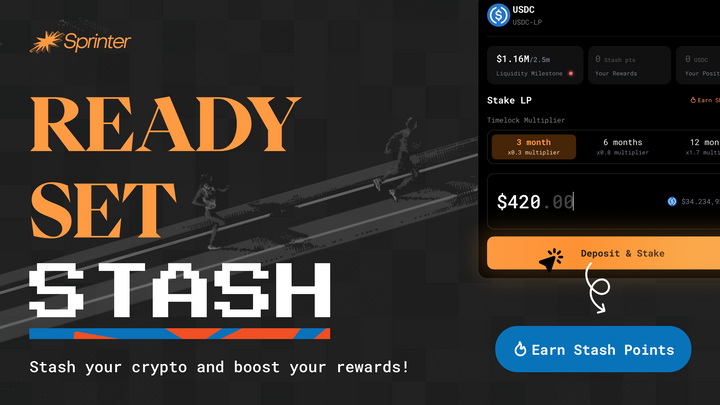

Sprinter Stash in this taxonomy: a non-deliverable, event-driven credit rail for cross-chain solvers, secured by guaranteed priority (repayment sink pays lender first) and guaranteed solvency (margin/limits/insurance). It converts LP stablecoin capital into on-demand credit that powers solver routes across chains, with LPs earning real yield from solver fees and safe passive sources.

With actors, the picture simplifies. We refer to the payer, who owes value, and the payee, who receives it. Depending on the mechanism, other roles attach: a lender/credit provider who advances funds so the payee needn’t wait; a risk engine that measures exposure and enforces margins and liquidations (a smart contract in DeFi, a CCP in TradFi); an escrow or oracle that locks value and proves conditions; a guarantor or insurance fund that absorbs tail events; and a venue, custodian, or settlement agent that executes or records transfers. Different combinations of these roles give each mechanism its distinctive risk shape.

A few practical questions help you choose. If a failed leg right now would cause irreparable harm and there is no credible recourse, you want instant exchange. If you can lock value and wait for proof, escrow buys safety without credit. If your flows are naturally batched and netted by the calendar, deferred settlement is efficient as long as priority is clear and the paying side can remain solvent until the window closes—either by its own strength or with a lender standing in. If exposures evolve with every price tick and moving cash that often is impractical, boundary settlement is appropriate, but only when solvency is guaranteed ahead of time and the order of payments at the boundary is indisputable. In markets where many parties face each other simultaneously, a CCP adds the discipline and efficiency of multilateral netting with a single, well‑capitalized risk manager.

In conclusion, the answer to the initial question, what we are pricing when we quote a rate, is expected loss, capital, and margin. Join us soon for Part II, which will ask a different question: while we wait for payment, how do we move value safely?

Make sure to stay tuned on all things Sprinter, and onchain credit, by following us on X, joining our Telegram, and reading more on our blog.

Join us to shape the future of onchain credit.